Scorecard & Risk Rule Module

The Scorecard & Risk Rules is extremely flexible and is configurable by the User. It provides a rating for the Borrower or Obligor and the Facility.

The Scorecard can contain quantitative and qualitative factors.

Quantitative Factors

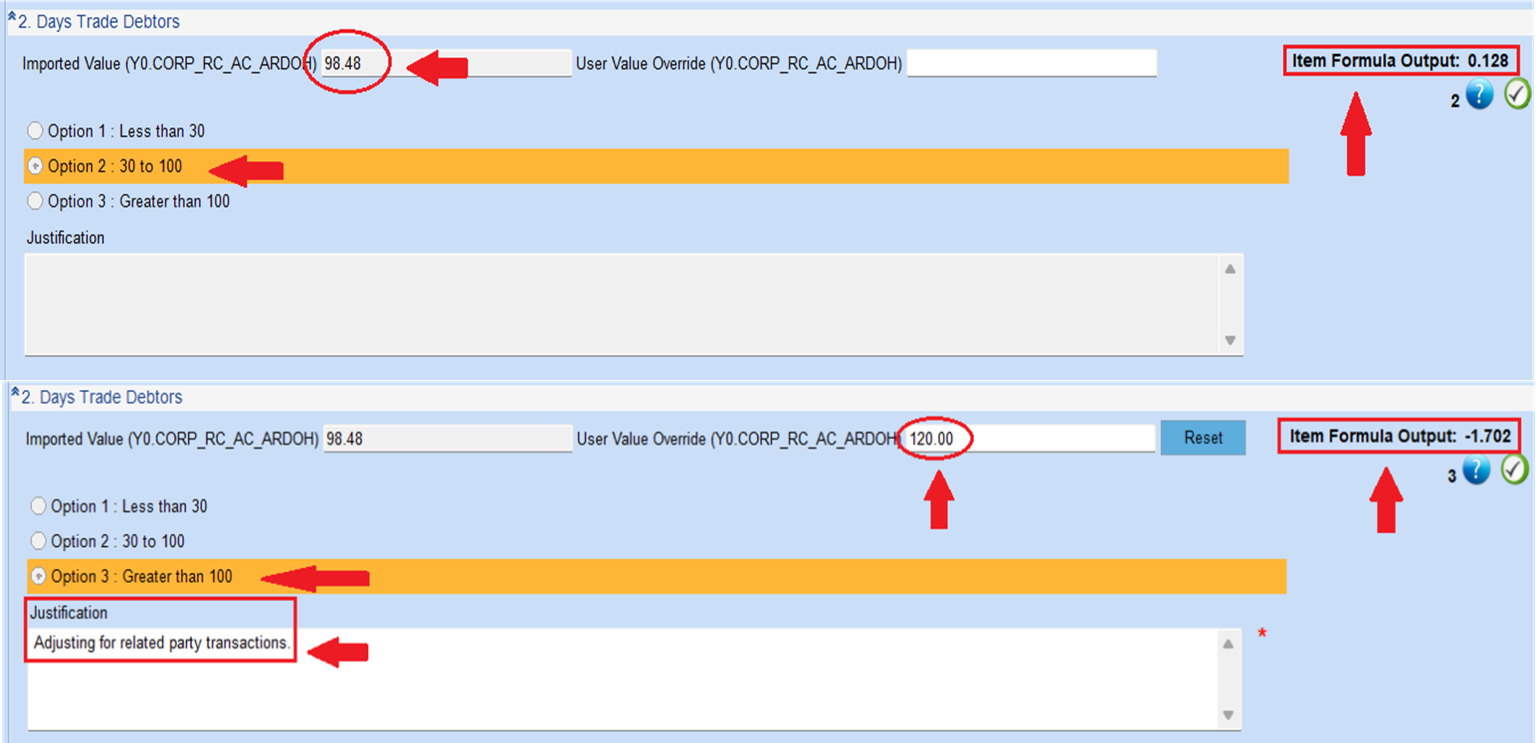

Quantitative Factors are usually the Financial Factors. The financial values are automatically mapped from financial spreadsheet “attached” to the Scorecard.

Financial value of the factors can be manually override. However, User will need to provide a reason for the override.

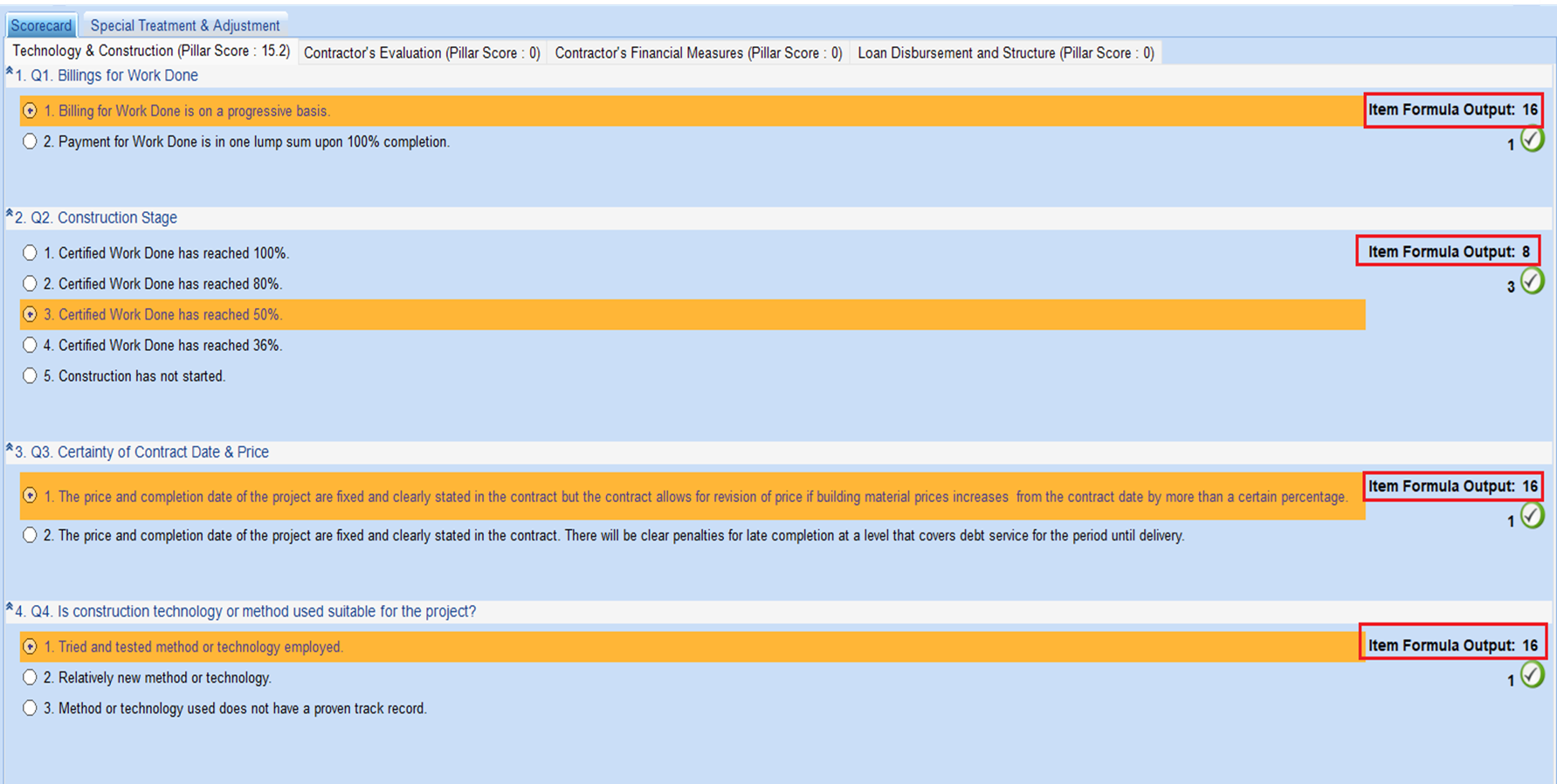

Qualitative Factors

For the qualitative factors, User selects the appropriate option by clicking on the radio button.

The scores of the selected option are displayed as “Item Formula Output” on the right-hand side of the screenshot.

External Data

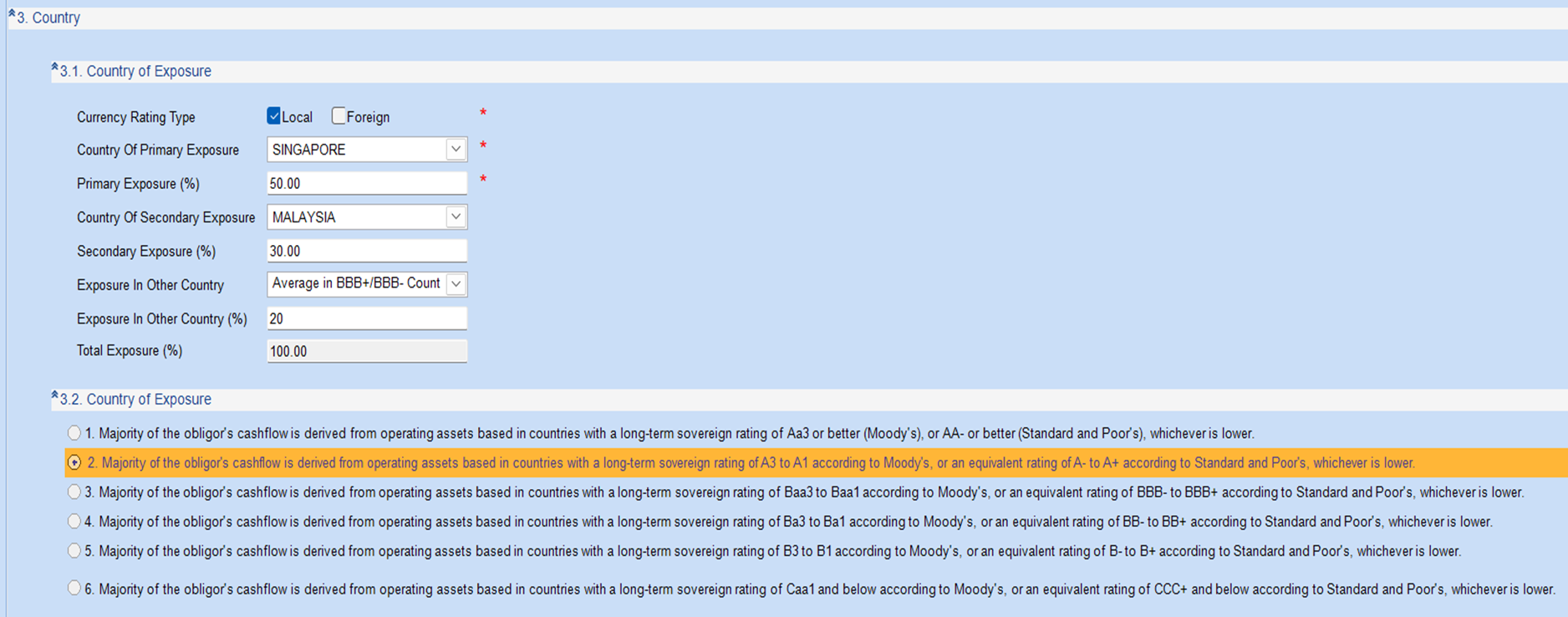

Our System supports the use of external data such as external ratings by Moody’s. S&P and Fitch in your Scorecard.

For example, User can incorporate Sovereign Ratings/Country Risks in their Scorecard.

Adjustments

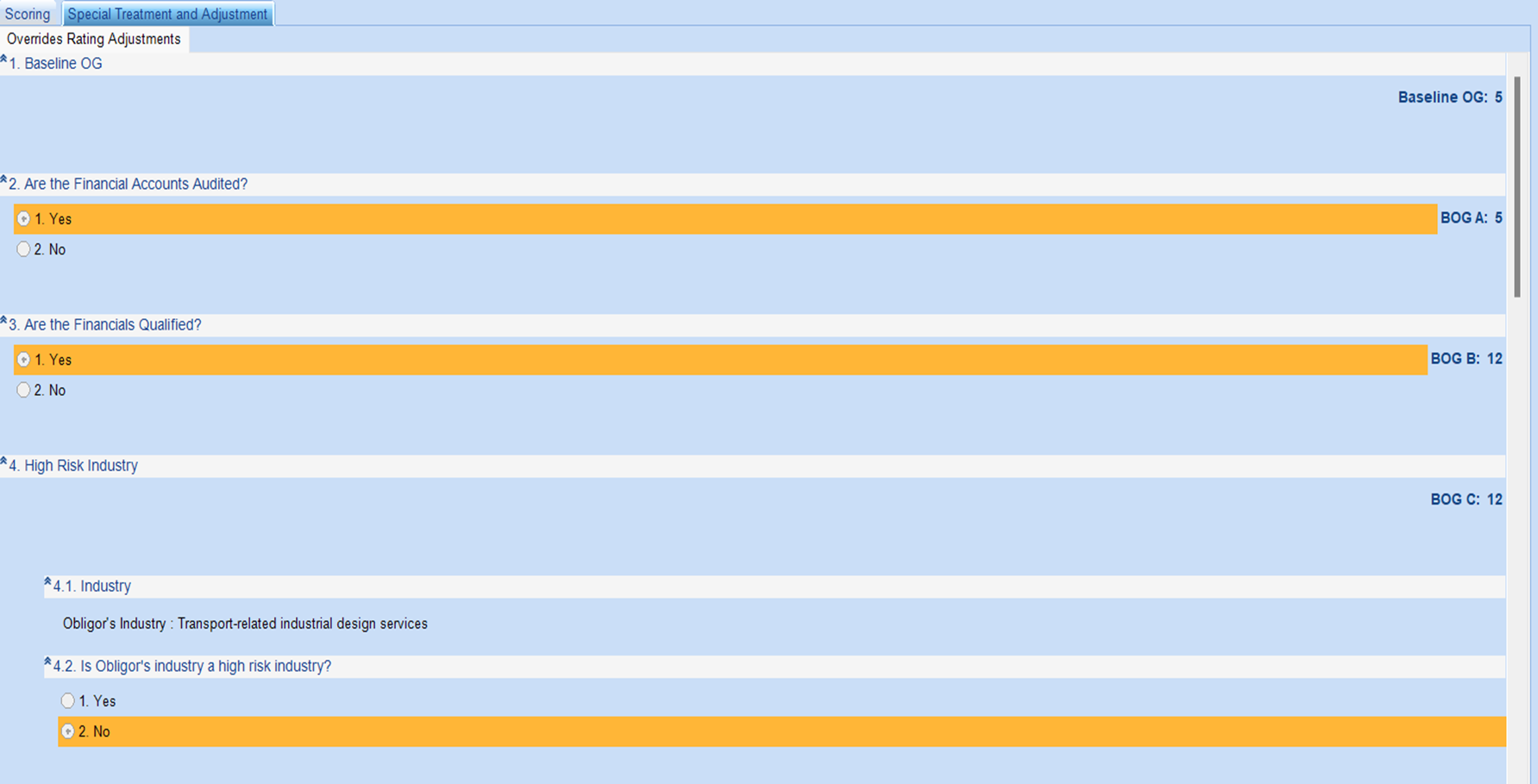

Our System has another feature of “Special Treatment and Overrides”. This is to cater for Adjustments to the Borrower’s Grade based on the Bank’s policies.

Examples of Adjustments are; "Are the Financial Accouns Audited?", "Are the Financials Qualified?" and "High Risk Industry".

Parent Support and Guarantor Support

User has the flexibility of incorporating Parent Support and Guarantor Support in their Scorecard.

Portfolio Stress Testing Module

Portfolio Stress Testing in Credit Predix empowers financial institutions to assess the resilience of their borrower portfolios under various "what-if" scenarios. Users can stress test the entire portfolio or a filtered subset based on criteria such as industry, business unit, team, or country. Testing can focus on borrowers' financial statements, scorecards, or both, providing flexibility and insights into potential risks.